By Dara Ajala-Damisa and Kemisola Agbaoye (Lead Writers)

Last Thursday evening, some great news was delivered to health advocates and Nigerians at large. The President had just signed to law an Act to repeal the National Health Insurance Scheme Act of 1999 and establish the National Health Insurance Authority.

For many who are keen followers of Nigeria’s journey to Universal Health Coverage, it could be said that this was one small step for legislation, one big step towards Universal Health Coverage in Nigeria because through the Act just signed by Mr President; health insurance was now mandatory for all Nigerians! This could mean that over 70% of Nigerians who pay for health out of pocket, many of whom are thrown into poverty as a result could benefit from national level mandatory health insurance.

As a quick digest, here are five things you need to know about the new National Health Insurance Authority Act of 2022;

- HEALTH INSURANCE IS NOW MANDATORY

Yes, every Nigerian is now mandated by law to get health insurance! Specifically, the Act requires the following to get health insurance:

- All employers and employees in the public and private sectors with five staff and above

- Informal sector employees, and

- All other residents in Nigeria

This is an improvement from the National Health Insurance Scheme Act, 2004 , 1999 whose purpose was “providing health insurance which shall entitle insured persons and their dependants the benefit of prescribed good quality and cost-effective health services”, and a major step towards the achievement of Universal Health Coverage (UHC).

2.FROM A SCHEME TO AN AUTHORITY — IMPLICATIONS

The National Health Insurance Scheme Act, 2004 established a scheme whose purpose was to provide health insurance to entitled insured persons and dependents.

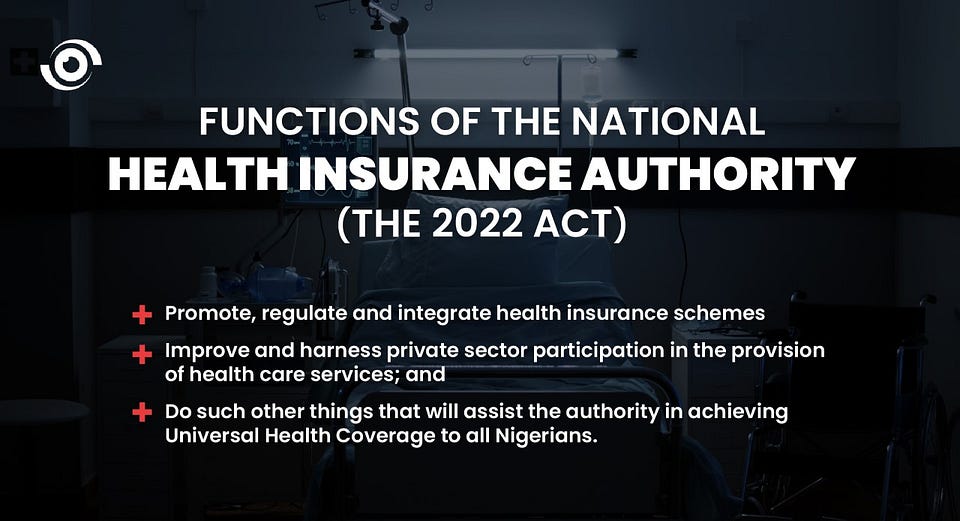

The National Health Insurance Authority Act, 2022 however created an oversight and regulatory body for Health Insurance Schemes and more clearly defined the roles of this authority to:

(a) Promote, regulate and integrate health insurance schemes;

(b) Improve and harness private sector participation in the provision of health care services; and

© Do such other things that will assist the authority in achieving Universal Health Coverage to all Nigerians.

One way the NHIA will likely integrate health insurance schemes in Nigeria is through an extensive information and data management system which the law stipulates should be established in collaboration with other information management organisations in Nigeria and across all states.

3. THIRD PARTY ADMINISTRATORS

Two components of the NHIA Act of 2022 speak to Third Party Administrators. The first expands the role of Third-Party Administrators and the second restricts the actions of Health Maintenance Organisations (HMOs). Considering how HMOs are in fact TPAs, these two stipulations might seem conflicting at first glance. But we break it down a little more below.

Expanded definition of Third-Party Administrators: First, Third Party Administrators (TPAs) are intermediaries to facilitate claims between the insurer and the insured.

TPAs were not defined or referred to in the NHIS Act, 1999. This gap meant that HMOs were the only acknowledged administrators of health insurance outside the National Scheme, limiting the efficacy of health service delivery. In the newly signed act, TPAs have been expanded to include: HMOs, Mutual Health Associations and other TPAs of health insurance.

TPAs are defined by the NHIA act of 2022 “any organisation with expertise and capability to administer all or a portion of the insurance claims process, including administration of claims, collection of premiums, enrolment and other administrative activities, which is registered by the Authority.”

Restricted scope of HMO services: An important aspect of the new law is how it limits the scope of HMOs in comparison with the NHIS Act of 1999. The previous NHIS Act had HMOs empowered to collect and implement contributions for premiums, including payment for services to healthcare providers, investment of pooled funds not in use etc. The Act establishing the NHIA however removes fund management completely from HMOs and places it with State Health Insurance Schemes (SHIS). Essentially, HMOs may collect contributions for premiums on behalf of SHIS where they are employed to do so but must remit these pooled funds to the SHIS who will then manage, and or invest the funds through the NHIA.

The new NHIA Act addressed a conflict of interest that existed in the NHIS Act, where the NHIS council included a Health Maintenance Organisation. This clearly stood in the way of proper regulation and monitoring of HMOs which ideally was part of the NHIS’ mandate, leading to allegations of abuse, monetary impropriety and fraud levelled against the HMOs and NHIS. The new act in no way has representatives of HMOs as part of its governing council. In fact, prospective council members are required to declare assets, and investment in any HMO is grounds for reconsidering such a member. That’s one way to be accountable.

The question to be asked is, are TPAs able to make healthcare more available, accessible and affordable to the population at large? This should be the underlying raison d’être for all of the new agency’s engagement with TPAs. Where wings are clipped or wings extended, NHIA’s mandate to provide mandatory quality services for all Nigerians without financial harm must remain paramount.

4. NHIA AS A REGULATOR, IMPLEMENTER, INVESTOR, AND INSURER

A summary of the new Act shows that the NHIA has been outfitted with a wide range of expanded functions that empower the Authority to serve as regulator, implementer, investor and insurer of health insurance practices and schemes in Nigeria.

NHIA as a Regulator — Given continued advocacy, intense technical and public sessions and debate, the new act clearly states that the NHIA is empowered to serve as regulator of Health Insurance Schemes in the country. As we have written about extensively, many state health insurance schemes have been established to provide services for residents. These needed a governing body that the NHIS was just not empowered by law to provide. Thus, the NHIA will now promote, regulate and integrate all health insurance schemes in Nigeria.

NHIA will also regulate, accredit and register HMOs and other third-party administrators since it has been empowered by this new act as a licensing body to carry out these oversight functions for TPAs.

NHIA as an Insurer — This new Act seeks to make NHIA a wholesome authority which will insure registered private health insurance companies through a security deposit that these HMOs are required to pay before registration. This function ensures that should a health insurance scheme or private health insurance organisation run into financial trouble or out of business for any reason, enrolees continue to remain insured and do not suffer financial ruin. Similar to how the Central Bank of Nigeria (CBN) and Nigeria Deposit Insurance Corporation (NDIC) insures banks to protect user funds.

NHIA as an investor — This simply empowers the NHIA to invest funds not in immediate use in approved federal government securities at the discretion of the governing council. Sustainability of funding for health insurance schemes continues to be the goal and it is expected that by investing funds at the NHIA level, schemes will have a support system for funding in emergency.

NHIA as an Implementer — This is one component of the new act that did not change much from the NHIS Act, 1999 and continues to raise questions among experts. Should a National Health Insurance Authority mandated with regulatory oversight for other schemes also implement health insurance by running a scheme?

This question was not answered in the new Act since the provisions state that NHIA will establish and run a scheme that provides health insurance for all employees in Federal Service. If all states plus the FCT are being empowered to establish health insurance schemes that will provide care for all residents in those locations, why create another fragmented pool for federal employees? Is it not safe to say that even federal employees reside in one of these 37 locations?

It is understandable however, how a separate scheme for federal employees may be more practicable for ease of premium contributions given the way federal employees’ salaries are structured and paid centrally. It is thus easier to deduct at source. Another option could be to make health insurance deductions for federal employees at source and then remit payments to corresponding State Health Insurance Schemes (same way other employers are required to). This will consolidate the State Health Insurance pools and free the NHIA to properly regulate Health Insurance in Nigeria.

5.FINANCIAL MANAGEMENT CHANGES

The new NHIA Act stipulates the creation of a new vulnerable group fund and retains the NHIA fund.

The Vulnerable Group Fund

The vulnerable group fund will be established to provide for

- Subsidy for health insurance coverage for vulnerable persons

- Payment of health insurance premiums for indigents

Just as interesting to note are the sources of this fund; the Basic Health Care Provision Fund (BHCPF), health insurance levy, special intervention fund allocated by the government, interests from investments and others — grants, donations, gifts and contributions. The telecom tax previously included in the bill was subsequently removed. It is worth asking how the funds would have been earmarked and managed for the provision of health insurance for the vulnerable — what mechanisms and instruments would have been put in place? Should this tax therefore not be included in the Finance Act instead?

This fund will be managed by the Governing Council through directives to the NHIA, and shall provide a formula for the disbursement of monies from the fund, and develop criteria for the disbursement of subsidies to State Health Insurance Schemes, subject to the approval of the Minister of Health.

One key point to note is the need for specifications on who the vulnerable and indigents that will benefit from this fund are. While the Act says it will be determined by the Governing Council (and that those who have private health insurance are not eligible to benefit from the fund), the specifics of who they are, needs to be clarified and put in the public domain.

The NHIA Fund

The new Act retains the NHIS fund stipulated in the 1999 NHIS Act. All expenditures shall be made from this fund, including staff salaries, allowances and benefits. It shall be funded by Federal Government allocations, donors, charges from private insurance, fees, fines and commissions, gifts and contributions. It can also be invested in securities and deposits, with interests accrued back to the fund. Proper accounts on the management of this fund will be presented to the Minister of Health not more than 6 months after the succeeding year. The NHIA also continues to be exempt from tax.

One other critical component of the Act to note is that NHIA is to undertake on its own or in collaboration with others sustained and continuous public education on health insurance. As we outline in this 2017 article, NHIA already has a ready group of collaborators in Universal Health Coverage advocates who have sustained continuous public education on health insurance across states and communities. One good example is Nigeria Health Watch’s Health4AllNaija advocacy which since 2017 has worked to drive citizens’ awareness around health insurance and its benefits to community members in various states while advocating for, and providing technical support around UHC legislation.

Ultimately, it is good to see that many of the critical recommendations made regarding the NHIS Act have been addressed in the NHIA Act. We will continue to monitor and support implementation to ensure that we achieve #Health4AllNaija.

What are your thoughts on the new NHIA act? Should NHIA implement a health insurance scheme? What stood out the most for you in the NHIA Act? We’d love to hear your thoughts! Let us know in the comments section below or join the conversation online using #Health4AllNaija.

Really informative. Thanks for the brief

What stood out for me in the new NHIA Act is the mandatory clause that makes it compulsory for all residents in Nigeria to have a health insurance cover..

NHIA should not implement a scheme. Doing so will encumber the Authority and distract it from its governance, oversight, investment and regulatory roles. More so, the reinsurance role for supplementory private health insurance schemes to be run by the HMOs is a critical and technical responsibility bestowed on the NHIA. The Authority should be more concerned on how to build its capacity that will guarantee the seamless implementation of all these new roles the NHIA Act has put on its shoulders than the business of implementing a scheme. This should be left in the hands of SHIS across the 36 states and FCT.

How can teachers in public private schools start to benefit from this

Public and private schools can access coverage for their staff. Individuals can also pay the premium to obtain coverage for themselves and their families. Please refer to http://www.nhis.gov.ng for more information.

The NHIA Act still has the telecoms tax. It has not been removed contrary to what your analysis or report said. Kindly obtain a copy of the Act and refer to Section 26, 1 (c).

The tax is “at least 1 kobo per every second of GSM calls”

Hi Dimeji,

Thanks for your comment. The telecom tax was indeed taken out of the Act before assent by Mr. President.

This is not going to end well, Government regulatory Bodies should focus on regulating and overseeing the implementation of laws in the health sector by private HMOs and not taking over Operational activities.

Saying all fund contributions should be remitted to the NHIA is just another avenue for fraud and corruption. Next we will hear is that cockroaches ate all the records.

By making the health insurance mandatory, it therefore means that it is compulsory for all Nigrians to have health insurance cover. What modalities does the Act have in place to ensure that all residents have access to the health benefits?

What parameters does the Act have in place to ensure the right persons benefit from the vulnerable group’s package?

NHIA as regulator should license all HMOs and Third Party Administrators recommended by the State Health Insurance Scheme.